All Categories

Featured

However, these plans can be a lot more complicated contrasted to other kinds of life insurance, and they aren't always best for every single capitalist. Talking with an experienced life insurance policy agent or broker can aid you make a decision if indexed global life insurance policy is an excellent suitable for you. Investopedia does not offer tax, investment, or monetary services and recommendations.

, including an irreversible life plan to their financial investment portfolio may make feeling.

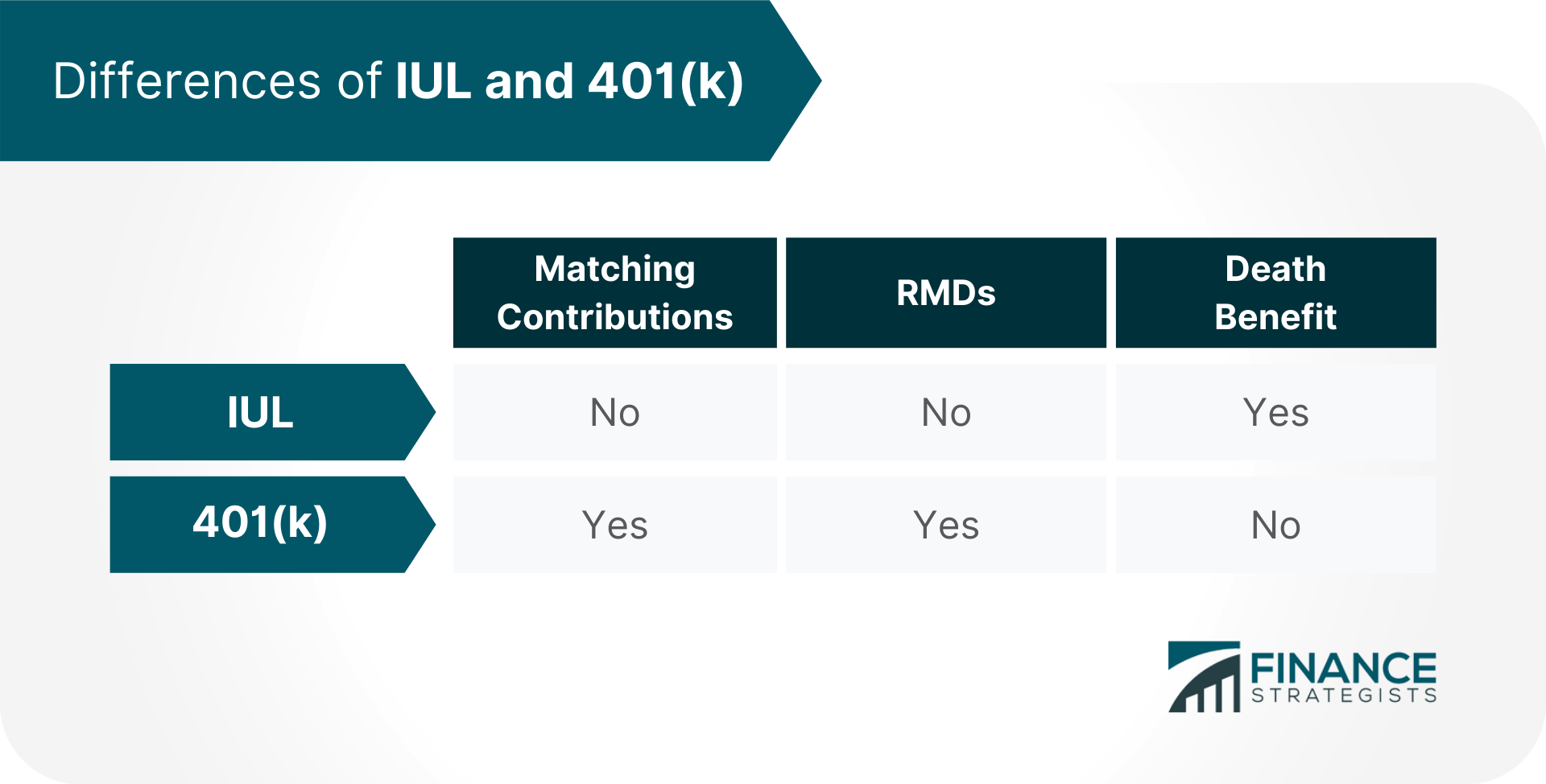

Low rates of return: Current study discovered that over a nine-year period, employee 401(k)s expanded by approximately 15.6% each year. Compare that to a set rates of interest of 2%-3% on a long-term life policy. These differences include up gradually. Applied to $50,000 in financial savings, the charges over would certainly equal $285 each year in a 401(k) vs.

In the same capillary, you could see financial investment development of $7,950 a year at 15.6% passion with a 401(k) contrasted to $1,500 annually at 3% interest, and you 'd invest $855 even more on life insurance policy each month to have whole life coverage. For lots of people, obtaining long-term life insurance coverage as component of a retired life plan is not an excellent idea.

Transamerica Financial Foundation Iul Reviews

Below are 2 common kinds of permanent life plans that can be made use of as an LIRP. Entire life insurance policy offers dealt with premiums and cash value that grows at a fixed rate set by the insurer. Traditional financial investment accounts normally supply greater returns and more adaptability than whole life insurance, yet whole life can give a reasonably low-risk supplement to these retired life savings methods, as long as you're confident you can afford the costs for the lifetime of the plan or in this instance, until retirement.

{kind=link}

Latest Posts

Universal Life Insurance Loans

Universal Life Insurance Calculator Cash Value

North American Universal Life Insurance